Unemployment

Did

you know that the total number of unemployed workers in G20 counties is

now up to 93 million and that it is increasing with each passing day?

You see, the truth is that the United States is not the only one dealing

with a systemic unemployment crisis. This is literally happening all

over the planet. So what is causing this crisis? Is there any hope

that it will be turned around? Well, unfortunately there are several

long-term trends that have been developing for decades that have played a

major role in bringing us to this point. First of all, the giant

corporations that now totally dominate the global economy have figured

out that they can make a lot more money by replacing expensive workers

that live in major industrialized nations with workers that live in

nations where it is legal to pay slave labor wages. So it isn't really a

huge mystery why there is such a huge problem with unemployment in the

western world. If you were running a giant corporation, why would you

want to hire workers that will cost you 10 to 20 times as much as other

workers? A worker is a worker, and over the past decade we have seen a

massive movement of jobs to countries where labor is cheaper. In

addition, large corporations are also trying to completely eliminate as

many jobs as they can by using technology. If a corporation can get a

computer or a machine or a robot to do a task more cheaply than a human

worker can do it, then why would that corporation want to continue to

rely on human labor? And of course we have seen an overall weakening of

the economies of the western world in recent years as well. This has

been particularly true in the United States. As these long-term trends intensify, the worldwide unemployment crisis is going to get even worse. (Read More....)

Did

you know that the total number of unemployed workers in G20 counties is

now up to 93 million and that it is increasing with each passing day?

You see, the truth is that the United States is not the only one dealing

with a systemic unemployment crisis. This is literally happening all

over the planet. So what is causing this crisis? Is there any hope

that it will be turned around? Well, unfortunately there are several

long-term trends that have been developing for decades that have played a

major role in bringing us to this point. First of all, the giant

corporations that now totally dominate the global economy have figured

out that they can make a lot more money by replacing expensive workers

that live in major industrialized nations with workers that live in

nations where it is legal to pay slave labor wages. So it isn't really a

huge mystery why there is such a huge problem with unemployment in the

western world. If you were running a giant corporation, why would you

want to hire workers that will cost you 10 to 20 times as much as other

workers? A worker is a worker, and over the past decade we have seen a

massive movement of jobs to countries where labor is cheaper. In

addition, large corporations are also trying to completely eliminate as

many jobs as they can by using technology. If a corporation can get a

computer or a machine or a robot to do a task more cheaply than a human

worker can do it, then why would that corporation want to continue to

rely on human labor? And of course we have seen an overall weakening of

the economies of the western world in recent years as well. This has

been particularly true in the United States. As these long-term trends intensify, the worldwide unemployment crisis is going to get even worse. (Read More....)[...]

A

fundamental shift is taking place in the U.S. economy. In fact, this

transition is rapidly picking up momentum and is in danger of becoming

an avalanche. The percentage of full-time jobs in our economy is

steadily declining and the percentage of part-time jobs is steadily

increasing. This is not a recent phenomenon, but now there are several

factors which are accelerating this trend. One of them is Obamacare.

The truth is that Obamacare actually gives business owners incentive to

cut hours and turn full-time workers into part-time workers, and according to the Wall Street Journal

and other prominent publications this is already happening all over the

United States. Perhaps this is part of the reasons why the U.S.

economy actually lost 240,000 full-time jobs last month. (Read More....)

A

fundamental shift is taking place in the U.S. economy. In fact, this

transition is rapidly picking up momentum and is in danger of becoming

an avalanche. The percentage of full-time jobs in our economy is

steadily declining and the percentage of part-time jobs is steadily

increasing. This is not a recent phenomenon, but now there are several

factors which are accelerating this trend. One of them is Obamacare.

The truth is that Obamacare actually gives business owners incentive to

cut hours and turn full-time workers into part-time workers, and according to the Wall Street Journal

and other prominent publications this is already happening all over the

United States. Perhaps this is part of the reasons why the U.S.

economy actually lost 240,000 full-time jobs last month. (Read More....)[...]

As

the number of good jobs continues to decline, the number of Americans

that cannot take care of themselves without government assistance

continues to explode. On Friday, we learned that the U.S. economy added

"195,000 jobs" last month. But when you look deeper at the numbers,

another story emerges. Last month, the U.S. economy actually lost 240,000 full-time jobs. Overall, the U.S. economy has only added 130,000 full-time jobs in 2013, but it takes about 90,000 full-time jobs a month

just to keep up with population growth. So we are losing quite a bit

of ground as far as full-time jobs are concerned. Meanwhile, the U.S.

economy has added more than 500,000 part-time jobs

so far this year. Unfortunately, there are very, very few part-time

and temp jobs that can be considered "breadwinner jobs". Part-time jobs

are great for teenagers, university students and elderly people that

only want to work a limited number of hours, but what most Americans

need are good paying full-time jobs with benefits that will allow them

to take care of their families. Unfortunately, those jobs are

continually becoming a smaller part of our economy. (Read More....)

As

the number of good jobs continues to decline, the number of Americans

that cannot take care of themselves without government assistance

continues to explode. On Friday, we learned that the U.S. economy added

"195,000 jobs" last month. But when you look deeper at the numbers,

another story emerges. Last month, the U.S. economy actually lost 240,000 full-time jobs. Overall, the U.S. economy has only added 130,000 full-time jobs in 2013, but it takes about 90,000 full-time jobs a month

just to keep up with population growth. So we are losing quite a bit

of ground as far as full-time jobs are concerned. Meanwhile, the U.S.

economy has added more than 500,000 part-time jobs

so far this year. Unfortunately, there are very, very few part-time

and temp jobs that can be considered "breadwinner jobs". Part-time jobs

are great for teenagers, university students and elderly people that

only want to work a limited number of hours, but what most Americans

need are good paying full-time jobs with benefits that will allow them

to take care of their families. Unfortunately, those jobs are

continually becoming a smaller part of our economy. (Read More....)[...]

Trying

to find a job in America today can be an incredibly frustrating

experience. Most of the jobs that are available seem to pay very

little, and there is intense competition for just about any job that is

open. But it wasn't always like this. When I was in high school, I was

immediately hired when I applied for a job at McDonalds because they

were so desperate for workers that they would hire just about anyone

that could flip a burger. But in this economic environment, a single nationwide hiring event conducted by McDonalds resulted in a million job applications,

and only a small percentage of those applicants were actually hired.

Our economy simply does not produce enough jobs for everyone anymore,

and the percentage of "good jobs" continues to decline. That means that

it is getting really hard to find a job that will enable you to support

a family, and a lot of people end up doing jobs that they are massively

overqualified for. But when times are tough, people are going to do

what they have to do in order to survive. (Read More....)

Trying

to find a job in America today can be an incredibly frustrating

experience. Most of the jobs that are available seem to pay very

little, and there is intense competition for just about any job that is

open. But it wasn't always like this. When I was in high school, I was

immediately hired when I applied for a job at McDonalds because they

were so desperate for workers that they would hire just about anyone

that could flip a burger. But in this economic environment, a single nationwide hiring event conducted by McDonalds resulted in a million job applications,

and only a small percentage of those applicants were actually hired.

Our economy simply does not produce enough jobs for everyone anymore,

and the percentage of "good jobs" continues to decline. That means that

it is getting really hard to find a job that will enable you to support

a family, and a lot of people end up doing jobs that they are massively

overqualified for. But when times are tough, people are going to do

what they have to do in order to survive. (Read More....)Banksters

Broke

nations are bailing out other broke nations with borrowed money. Round

and round we go - where we stop nobody knows. As of April, 41 different countries

had active financial "arrangements" with the IMF. Sometimes they are

called "bailouts" and sometimes they are called other things, but in

every single case they involve loans. And most of the time, these loans

come with very stringent conditions. It is a form of "global

governance" that most people don't even know about. For decades, the

IMF has been able to use money as a way to force developing nations to

do what it wants them to do. But up until fairly recently, this had

mostly only been done with poor nations. But now an increasing number

of wealthy nations are turning to the IMF for help. We have already

seen Greece, Portugal, Ireland and Cyprus receive bailouts which were

partly funded by the IMF, Spain has received a bailout for its banking

sector, and as I noted yesterday, it is being projected that Italy will need a major bailout within six months. How long can this go on before the entire system collapses? (Read More....)

Broke

nations are bailing out other broke nations with borrowed money. Round

and round we go - where we stop nobody knows. As of April, 41 different countries

had active financial "arrangements" with the IMF. Sometimes they are

called "bailouts" and sometimes they are called other things, but in

every single case they involve loans. And most of the time, these loans

come with very stringent conditions. It is a form of "global

governance" that most people don't even know about. For decades, the

IMF has been able to use money as a way to force developing nations to

do what it wants them to do. But up until fairly recently, this had

mostly only been done with poor nations. But now an increasing number

of wealthy nations are turning to the IMF for help. We have already

seen Greece, Portugal, Ireland and Cyprus receive bailouts which were

partly funded by the IMF, Spain has received a bailout for its banking

sector, and as I noted yesterday, it is being projected that Italy will need a major bailout within six months. How long can this go on before the entire system collapses? (Read More....)[...]

According to a study that was just released by Boston Consulting Group, the wealthiest one percent now own 39 percent of all the wealth in the world. Meanwhile, the bottom 50 percent only own 1 percent of all the wealth in the world combined.

The global financial system has been designed to funnel wealth to the

very top, and the gap between the wealthy and the poor continues to

expand at a frightening pace. The global elite continue to hoard wealth

and heap together enormous mountains of treasure in these troubled days

even though the economic suffering around the planet continues to

grow. So exactly how have the global elite accumulated so much wealth?

Well, one of the primary ways is through the use of debt. As I have

written about previously,

there is about 190 trillion dollars of debt in the world but global GDP

is only about 70 trillion dollars. Our debt-based global financial

system systematically transfers wealth from us and our governments into

the hands of the global elite. And of course the gigantic banks and

corporations that the elite control are constantly gobbling up

everything of value that they can find: natural resources, profitable

small businesses, real estate, politicians, etc. Money, power,

ownership and control are becoming very, very tightly concentrated at

the top of the food chain, and that is a very dangerous thing for

humanity. When too much money and power gets into too few hands, it

almost always results in tyranny. (Read More....)

According to a study that was just released by Boston Consulting Group, the wealthiest one percent now own 39 percent of all the wealth in the world. Meanwhile, the bottom 50 percent only own 1 percent of all the wealth in the world combined.

The global financial system has been designed to funnel wealth to the

very top, and the gap between the wealthy and the poor continues to

expand at a frightening pace. The global elite continue to hoard wealth

and heap together enormous mountains of treasure in these troubled days

even though the economic suffering around the planet continues to

grow. So exactly how have the global elite accumulated so much wealth?

Well, one of the primary ways is through the use of debt. As I have

written about previously,

there is about 190 trillion dollars of debt in the world but global GDP

is only about 70 trillion dollars. Our debt-based global financial

system systematically transfers wealth from us and our governments into

the hands of the global elite. And of course the gigantic banks and

corporations that the elite control are constantly gobbling up

everything of value that they can find: natural resources, profitable

small businesses, real estate, politicians, etc. Money, power,

ownership and control are becoming very, very tightly concentrated at

the top of the food chain, and that is a very dangerous thing for

humanity. When too much money and power gets into too few hands, it

almost always results in tyranny. (Read More....)[...]

Basel III: How The Bank For International Settlements Is Going To Help Bring Down The Global Economy

A

new set of regulations that most people have never even heard of that

was developed by an immensely powerful central banking organization that

most people do not even know exists is going to have a dramatic effect

on the global financial system over the next several years. The new set

of regulations is known as "Basel III", and it was developed by the

Bank for International Settlements. The Bank for International

Settlements has been called "the central bank for central banks", and it

is headquartered in Basel, Switzerland. 58 major central banks

(including the Federal Reserve) belong to the Bank for International

Settlements, and the decisions made in Basel often have more of an

impact on the direction of the global economy than anything the

president of the United States or the U.S. Congress are doing. All you

have to do is to look back at the last financial crisis to see an

example of this. Basel II and Basel 2.5 played a major role in

precipitating the subprime mortgage meltdown. Now a new set of

regulations known as "Basel III" are being rolled out. The

implementation of these new regulations is beginning this year, and they

will be completely phased in by 2019. These new regulations

dramatically increase capital requirements and significantly restrict

the use of leverage. Those certainly sound like good goals, the problem

is that the entire global financial system is based on credit at this

point, and these new regulations are going to substantially reduce the

flow of credit. The only way that the giant debt bubble that we are all

living in can continue to persist is if it continues to expand. By

restricting the flow of credit, these new regulations threaten to burst

the debt bubble and bring down the entire global economy. (Read More....)

A

new set of regulations that most people have never even heard of that

was developed by an immensely powerful central banking organization that

most people do not even know exists is going to have a dramatic effect

on the global financial system over the next several years. The new set

of regulations is known as "Basel III", and it was developed by the

Bank for International Settlements. The Bank for International

Settlements has been called "the central bank for central banks", and it

is headquartered in Basel, Switzerland. 58 major central banks

(including the Federal Reserve) belong to the Bank for International

Settlements, and the decisions made in Basel often have more of an

impact on the direction of the global economy than anything the

president of the United States or the U.S. Congress are doing. All you

have to do is to look back at the last financial crisis to see an

example of this. Basel II and Basel 2.5 played a major role in

precipitating the subprime mortgage meltdown. Now a new set of

regulations known as "Basel III" are being rolled out. The

implementation of these new regulations is beginning this year, and they

will be completely phased in by 2019. These new regulations

dramatically increase capital requirements and significantly restrict

the use of leverage. Those certainly sound like good goals, the problem

is that the entire global financial system is based on credit at this

point, and these new regulations are going to substantially reduce the

flow of credit. The only way that the giant debt bubble that we are all

living in can continue to persist is if it continues to expand. By

restricting the flow of credit, these new regulations threaten to burst

the debt bubble and bring down the entire global economy. (Read More....)[...]

Recently

uncovered documents prove that the Obama administration has been

working with the Mexican government to increase the number of illegal

immigrants on food stamps, and when more illegal immigrants go on food

stamps JP Morgan makes more money. As you will read about below, JP

Morgan has made at least 560 million dollars processing

Electronic Benefits Transfer cards. Each month, JP Morgan makes

between $.31 and $2.30 for every single person on food stamps (and that

does not even include things like ATM fees, etc). So JP Morgan has a

vested interest in seeing poverty grow and the number of people on food

stamps increase. Meanwhile, the Obama administration has been

aggressively seeking to expand participation in the food stamp program.

Under Obama, the number of people on food stamps has grown from 32

million to more than 47 million. And even though poverty in America is absolutely exploding,

that apparently is not good enough for the Obama administration. It

has now come out that the U.S. Department of Agriculture has provided

the Mexican government with literature that actively encourages illegal

immigrants to enroll in food stamps. One flyer contains the following

statement in Spanish: "You need not divulge information regarding your immigration status in seeking this benefit for your children."

The bold and the underlining are in the original document in case you

were wondering. Overall, federal spending on food stamps increased from

18 billion dollars in 2000 to 85 billion dollars in 2012, and at this

point one out of every five U.S. households

in now enrolled in the food stamp program. When people illegally or

fraudulently enroll in the food stamp program, it makes it harder for

those that desperately need the help to be able to get it. (Read More....)

Recently

uncovered documents prove that the Obama administration has been

working with the Mexican government to increase the number of illegal

immigrants on food stamps, and when more illegal immigrants go on food

stamps JP Morgan makes more money. As you will read about below, JP

Morgan has made at least 560 million dollars processing

Electronic Benefits Transfer cards. Each month, JP Morgan makes

between $.31 and $2.30 for every single person on food stamps (and that

does not even include things like ATM fees, etc). So JP Morgan has a

vested interest in seeing poverty grow and the number of people on food

stamps increase. Meanwhile, the Obama administration has been

aggressively seeking to expand participation in the food stamp program.

Under Obama, the number of people on food stamps has grown from 32

million to more than 47 million. And even though poverty in America is absolutely exploding,

that apparently is not good enough for the Obama administration. It

has now come out that the U.S. Department of Agriculture has provided

the Mexican government with literature that actively encourages illegal

immigrants to enroll in food stamps. One flyer contains the following

statement in Spanish: "You need not divulge information regarding your immigration status in seeking this benefit for your children."

The bold and the underlining are in the original document in case you

were wondering. Overall, federal spending on food stamps increased from

18 billion dollars in 2000 to 85 billion dollars in 2012, and at this

point one out of every five U.S. households

in now enrolled in the food stamp program. When people illegally or

fraudulently enroll in the food stamp program, it makes it harder for

those that desperately need the help to be able to get it. (Read More....)[...]

Economic Despair

The pension nightmare that is at the heart of the horrific financial crisis in Detroit is just the tip of the iceberg of the coming retirement crisis that will shake America to the core. Right now, more than 10,000 Baby Boomers

are hitting the age of 65 every single day, and this will continue to

happen every single day until the year 2030. As a society, we have made

trillions of dollars of financial promises to these Baby Boomers, and

there is no way that we are going to be able to keep those promises.

The money simply is not there. Yes, I suppose that we could eventually

see a "super devaluation" of the U.S. dollar and keep our promises to

the Baby Boomers using currency that is not worth much more than

Monopoly money, but as it stands right now we simply do not have the

resources to do what we said that we were going to do. The number of

senior citizens in the United States is projected to more than double by

the middle of the century, and it would have been nearly impossible to

support them all even if we weren't in the midst of a long-term economic decline.

Tens of millions of Americans that are eagerly looking forward to

retirement are going to be in for a very rude awakening in the years

ahead. There is going to be a lot of heartache and a lot of broken

promises. (Read More....)

The pension nightmare that is at the heart of the horrific financial crisis in Detroit is just the tip of the iceberg of the coming retirement crisis that will shake America to the core. Right now, more than 10,000 Baby Boomers

are hitting the age of 65 every single day, and this will continue to

happen every single day until the year 2030. As a society, we have made

trillions of dollars of financial promises to these Baby Boomers, and

there is no way that we are going to be able to keep those promises.

The money simply is not there. Yes, I suppose that we could eventually

see a "super devaluation" of the U.S. dollar and keep our promises to

the Baby Boomers using currency that is not worth much more than

Monopoly money, but as it stands right now we simply do not have the

resources to do what we said that we were going to do. The number of

senior citizens in the United States is projected to more than double by

the middle of the century, and it would have been nearly impossible to

support them all even if we weren't in the midst of a long-term economic decline.

Tens of millions of Americans that are eagerly looking forward to

retirement are going to be in for a very rude awakening in the years

ahead. There is going to be a lot of heartache and a lot of broken

promises. (Read More....)[...]

It

is so sad to watch one of America's greatest cities die a horrible

death. Once upon a time, the city of Detroit was a teeming metropolis

of 1.8 million people and it had the highest per capita income in the

United States. Now it is a rotting, decaying hellhole of about 700,000

people that the rest of the world makes jokes about. On Thursday, we

learned that the decision had been made for the city of Detroit to

formally file for Chapter 9 bankruptcy. It was going to be the largest

municipal bankruptcy in the history of the United States by far, but on

Friday it was stopped at least temporarily by an Ingham County judge.

She ruled that Detroit's bankruptcy filing violates the Michigan Constitution

because it would result in reduced pension payments for retired

workers. She also stated that Detroit's bankruptcy filing was "also not honoring the (United States) president, who took (Detroit’s auto companies) out of bankruptcy",

and she ordered that a copy of her judgment be sent to Barack Obama.

How "honoring the president" has anything to do with the bankruptcy of

Detroit is a bit of a mystery, but what that judge has done is ensured

that there will be months of legal wrangling ahead over Detroit's money

woes. It will be very interesting to see how all of this plays out.

But one thing is for sure - the city of Detroit is flat broke. One of

the greatest cities in the history of the world is just a shell of its

former self. The following are 25 facts about the fall of Detroit that

will leave you shaking your head... (Read More....)

It

is so sad to watch one of America's greatest cities die a horrible

death. Once upon a time, the city of Detroit was a teeming metropolis

of 1.8 million people and it had the highest per capita income in the

United States. Now it is a rotting, decaying hellhole of about 700,000

people that the rest of the world makes jokes about. On Thursday, we

learned that the decision had been made for the city of Detroit to

formally file for Chapter 9 bankruptcy. It was going to be the largest

municipal bankruptcy in the history of the United States by far, but on

Friday it was stopped at least temporarily by an Ingham County judge.

She ruled that Detroit's bankruptcy filing violates the Michigan Constitution

because it would result in reduced pension payments for retired

workers. She also stated that Detroit's bankruptcy filing was "also not honoring the (United States) president, who took (Detroit’s auto companies) out of bankruptcy",

and she ordered that a copy of her judgment be sent to Barack Obama.

How "honoring the president" has anything to do with the bankruptcy of

Detroit is a bit of a mystery, but what that judge has done is ensured

that there will be months of legal wrangling ahead over Detroit's money

woes. It will be very interesting to see how all of this plays out.

But one thing is for sure - the city of Detroit is flat broke. One of

the greatest cities in the history of the world is just a shell of its

former self. The following are 25 facts about the fall of Detroit that

will leave you shaking your head... (Read More....)[...]

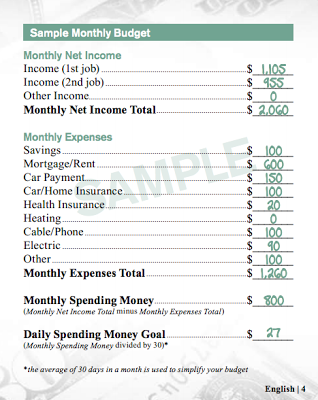

Can

you support a family on $2,000 a month? Recently, McDonald's and Visa

teamed up to launch a website that is intended to help employees of

McDonald's manage their money. The aspect of the website that is

getting a tremendous amount of national attention is the "McDonald's

Budget" which is a sample monthly budget which is designed to help

workers plan their spending. You can see a copy of it for yourself right here.

This budget is laughably unrealistic, but it is also deeply tragic,

because there are tens of millions of American workers that are actually

trying to raise families on this kind of an income. (Read More....)

Can

you support a family on $2,000 a month? Recently, McDonald's and Visa

teamed up to launch a website that is intended to help employees of

McDonald's manage their money. The aspect of the website that is

getting a tremendous amount of national attention is the "McDonald's

Budget" which is a sample monthly budget which is designed to help

workers plan their spending. You can see a copy of it for yourself right here.

This budget is laughably unrealistic, but it is also deeply tragic,

because there are tens of millions of American workers that are actually

trying to raise families on this kind of an income. (Read More....)[...]

Federal Reserve

Federal

Reserve Chairman Ben Bernanke said this week that inflation in the

United States needs to be higher. Yes, he actually came right out and

said that. It almost seems as if Bernanke is trying to purposely hurt

the middle class. On Wednesday, Bernanke told the press that "both sides of our mandate are saying we need to be more accommodative".

Of course he was referring to the Fed's dual mandate to keep

unemployment and inflation low, but Bernanke has a very unique

interpretation of that mandate. According to Bernanke, inflation in the

U.S. is now "too low".

The official inflation rate is currently sitting at about 1 percent,

and Bernanke insists that such a low rate of inflation is not good for the economy.

He would prefer that the rate of inflation be up around 2 percent, and

he is hoping that more "monetary accommodation" will help push inflation

up and the unemployment rate down. (Read More....)

Federal

Reserve Chairman Ben Bernanke said this week that inflation in the

United States needs to be higher. Yes, he actually came right out and

said that. It almost seems as if Bernanke is trying to purposely hurt

the middle class. On Wednesday, Bernanke told the press that "both sides of our mandate are saying we need to be more accommodative".

Of course he was referring to the Fed's dual mandate to keep

unemployment and inflation low, but Bernanke has a very unique

interpretation of that mandate. According to Bernanke, inflation in the

U.S. is now "too low".

The official inflation rate is currently sitting at about 1 percent,

and Bernanke insists that such a low rate of inflation is not good for the economy.

He would prefer that the rate of inflation be up around 2 percent, and

he is hoping that more "monetary accommodation" will help push inflation

up and the unemployment rate down. (Read More....)[...]

Did you know that U.S. banks have more than 1.8 trillion dollars parked at the Federal Reserve and that the Fed is actually paying them

not to lend that money to us? We were always told that the goal of

quantitative easing was to "help the economy", but the truth is that the

vast majority of the money that the Fed has created through

quantitative easing has not even gotten into the system. Instead, most

of it is sitting at the Fed slowly earning interest for the bankers.

Back in October 2008, just as the last financial crisis was starting,

Federal Reserve Chairman Ben Bernanke announced that the Federal Reserve

would start paying interest on the reserves that banks keep at the

Fed. This caused an absolute explosion in the size of these reserves.

Back in 2008, U.S. banks had less than 2 billion dollars

of excess reserves parked at the Fed. Today, they have more than 1.8

trillion. In less than five years, the pile of excess reserves has

gotten nearly 1,000 times larger. This is utter insanity, and it will have very serious consequences down the road. (Read More....)

Did you know that U.S. banks have more than 1.8 trillion dollars parked at the Federal Reserve and that the Fed is actually paying them

not to lend that money to us? We were always told that the goal of

quantitative easing was to "help the economy", but the truth is that the

vast majority of the money that the Fed has created through

quantitative easing has not even gotten into the system. Instead, most

of it is sitting at the Fed slowly earning interest for the bankers.

Back in October 2008, just as the last financial crisis was starting,

Federal Reserve Chairman Ben Bernanke announced that the Federal Reserve

would start paying interest on the reserves that banks keep at the

Fed. This caused an absolute explosion in the size of these reserves.

Back in 2008, U.S. banks had less than 2 billion dollars

of excess reserves parked at the Fed. Today, they have more than 1.8

trillion. In less than five years, the pile of excess reserves has

gotten nearly 1,000 times larger. This is utter insanity, and it will have very serious consequences down the road. (Read More....)[...]

What

does it look like when a 30 year bull market ends abruptly? What

happens when bond yields start doing things that they haven't done in 50 years?

If your answer to those questions involves the word "slaughter", you

are probably on the right track. Right now, bonds are being absolutely

slaughtered, and this is only just the beginning. Over the last several

years, reckless bond buying by the Federal Reserve has forced yields

down to absolutely ridiculous levels. For example, it simply is not

rational to lend the U.S. government money at less than 3 percent when

the real rate of inflation is somewhere up around 8 to 10 percent.

But when he originally announced the quantitative easing program,

Federal Reserve Chairman Ben Bernanke said that he intended to force

interest rates to go down, and lots of bond investors made a lot of

money riding the bubble that Bernanke created. But now that Bernanke

has indicated that the bond buying will be coming to an end, investors

are going into panic mode and the bond bubble is starting to burst. One

hedge fund executive told CNBC

that the "feeling you are getting out there is that people are selling

first and asking questions later". And the yield on 10 year U.S.

Treasuries just keeps going up. Today it closed at 2.59 percent,

and many believe that it is going to go much higher unless the Fed

intervenes. If the Fed does not intervene and allows the bubble that it

has created to burst, we are going to see unprecedented carnage. (Read More....)

What

does it look like when a 30 year bull market ends abruptly? What

happens when bond yields start doing things that they haven't done in 50 years?

If your answer to those questions involves the word "slaughter", you

are probably on the right track. Right now, bonds are being absolutely

slaughtered, and this is only just the beginning. Over the last several

years, reckless bond buying by the Federal Reserve has forced yields

down to absolutely ridiculous levels. For example, it simply is not

rational to lend the U.S. government money at less than 3 percent when

the real rate of inflation is somewhere up around 8 to 10 percent.

But when he originally announced the quantitative easing program,

Federal Reserve Chairman Ben Bernanke said that he intended to force

interest rates to go down, and lots of bond investors made a lot of

money riding the bubble that Bernanke created. But now that Bernanke

has indicated that the bond buying will be coming to an end, investors

are going into panic mode and the bond bubble is starting to burst. One

hedge fund executive told CNBC

that the "feeling you are getting out there is that people are selling

first and asking questions later". And the yield on 10 year U.S.

Treasuries just keeps going up. Today it closed at 2.59 percent,

and many believe that it is going to go much higher unless the Fed

intervenes. If the Fed does not intervene and allows the bubble that it

has created to burst, we are going to see unprecedented carnage. (Read More....)[...]

Did

you know that you are involved in the most massive Ponzi scheme that

has ever existed? To illustrate my point, allow me to tell you a little

story. Once upon a time, there was a man named Sam. When he was

younger, he had been a very principled young man that had worked

incredibly hard and that had built a large number of tremendously

successful businesses. He became fabulously wealthy and he accumulated

far more gold than anyone else on the planet. But when he started to

get a little older he forgot the values of his youth. He started making

really bad decisions and some of his relatives started to take

advantage of him. One particularly devious relative was a nephew named

Fred. One day Fred approached his uncle Sam with a scheme that his

friends the bankers had come up with. What happened next would change

the course of Sam's life forever. (Read More....)

Did

you know that you are involved in the most massive Ponzi scheme that

has ever existed? To illustrate my point, allow me to tell you a little

story. Once upon a time, there was a man named Sam. When he was

younger, he had been a very principled young man that had worked

incredibly hard and that had built a large number of tremendously

successful businesses. He became fabulously wealthy and he accumulated

far more gold than anyone else on the planet. But when he started to

get a little older he forgot the values of his youth. He started making

really bad decisions and some of his relatives started to take

advantage of him. One particularly devious relative was a nephew named

Fred. One day Fred approached his uncle Sam with a scheme that his

friends the bankers had come up with. What happened next would change

the course of Sam's life forever. (Read More....)Housing Crash

Did

you actually think that mortgage rates were going to stay at all-time

lows forever? Federal Reserve Chairman Ben Bernanke was able to grossly

distort the market for a while by buying up massive amounts of

government bonds and mortgage-backed securities, but there was no way in

the world that the market was going to stay that distorted forever. It

simply does not make sense to give American families 30 year mortgages

at a fixed interest rate of less than four percent when the real rate of

inflation is somewhere around eight to ten percent and the mortgage

delinquency rate in the United States is 9.72 percent.

If we actually did have "free markets" and they were behaving

rationally, mortgage rates would be far, far higher. Well, now that the

Fed has indicated that they are going to be starting to "taper" QE at

some point, bond yields have skyrocketed

and this is rapidly pushing up mortgage rates. According to Freddie

Mac, we just witnessed the largest weekly increase in mortgage rates in

26 years. Sadly, this is only just the beginning. Unless the Federal

Reserve intervenes, mortgage rates are going to continue to try to

revert to normal. (Read More....)

Did

you actually think that mortgage rates were going to stay at all-time

lows forever? Federal Reserve Chairman Ben Bernanke was able to grossly

distort the market for a while by buying up massive amounts of

government bonds and mortgage-backed securities, but there was no way in

the world that the market was going to stay that distorted forever. It

simply does not make sense to give American families 30 year mortgages

at a fixed interest rate of less than four percent when the real rate of

inflation is somewhere around eight to ten percent and the mortgage

delinquency rate in the United States is 9.72 percent.

If we actually did have "free markets" and they were behaving

rationally, mortgage rates would be far, far higher. Well, now that the

Fed has indicated that they are going to be starting to "taper" QE at

some point, bond yields have skyrocketed

and this is rapidly pushing up mortgage rates. According to Freddie

Mac, we just witnessed the largest weekly increase in mortgage rates in

26 years. Sadly, this is only just the beginning. Unless the Federal

Reserve intervenes, mortgage rates are going to continue to try to

revert to normal. (Read More....)[...]

Federal

Reserve Chairman Ben Bernanke has done it. He has succeeded in

creating a new housing bubble. By driving mortgage rates down to the

lowest level in 100 years and recklessly printing money with wild

abandon, Bernanke has been able to get housing prices to rebound a bit.

In fact, in some of the more prosperous areas of the country you would

be tempted to think that it is 2005 all over again. If you can believe

it, in some areas of the country builders are actually holding lotteries

to see who will get the chance to buy their homes. Wow - that sounds

great, right? Unfortunately, this "housing recovery" is not based on

solid economic fundamentals. As you will see below, this is a recovery

that is being led by investors. They are paying cash for cheap

properties that they believe will appreciate rapidly in the coming

years. Meanwhile, the homeownership rate in the United States continues

to decline. It is now the lowest that it has been since 1995. There are a couple of reasons for this. Number one, there has not been a jobs recovery in the United States. The percentage of working age Americans with a job has not rebounded at all and is still about the exact same place where it was at the end of the last recession. Secondly, crippling levels of student loan debt

continue to drive down the percentage of young people that are buying

homes. So no, this is not a real housing recovery. It is an

investor-led recovery that is mostly limited to the more prosperous

areas of the country. For example, the median sale price of a home in

Washington D.C. just hit a new all-time record high. But this bubble will not last, and when this new housing bubble does burst, will it end as badly as the last one did? (Read More....)

Federal

Reserve Chairman Ben Bernanke has done it. He has succeeded in

creating a new housing bubble. By driving mortgage rates down to the

lowest level in 100 years and recklessly printing money with wild

abandon, Bernanke has been able to get housing prices to rebound a bit.

In fact, in some of the more prosperous areas of the country you would

be tempted to think that it is 2005 all over again. If you can believe

it, in some areas of the country builders are actually holding lotteries

to see who will get the chance to buy their homes. Wow - that sounds

great, right? Unfortunately, this "housing recovery" is not based on

solid economic fundamentals. As you will see below, this is a recovery

that is being led by investors. They are paying cash for cheap

properties that they believe will appreciate rapidly in the coming

years. Meanwhile, the homeownership rate in the United States continues

to decline. It is now the lowest that it has been since 1995. There are a couple of reasons for this. Number one, there has not been a jobs recovery in the United States. The percentage of working age Americans with a job has not rebounded at all and is still about the exact same place where it was at the end of the last recession. Secondly, crippling levels of student loan debt

continue to drive down the percentage of young people that are buying

homes. So no, this is not a real housing recovery. It is an

investor-led recovery that is mostly limited to the more prosperous

areas of the country. For example, the median sale price of a home in

Washington D.C. just hit a new all-time record high. But this bubble will not last, and when this new housing bubble does burst, will it end as badly as the last one did? (Read More....)[...]

New

home sales in the United States are on pace to set a brand new all-time

record low in 2011. This will be the third year in a row that new home

sales have set a new record low. Sadly, this is yet another sign that

the U.S. economy continues to grow weaker. Back in 2005, more than four

times as many new homes were being sold as are being sold today. The

home building industry is one of the central pillars of the U.S.

economy, and the fact that we are going to set another new record low

for home sales in 2011 is a really bad sign for those hoping for an

economic recovery. Unlike most of those that work in the financial

industry, those that build new homes produce something of lasting value

for American families. In addition, millions of Americans have

traditionally made a solid living by building and selling new homes.

But today the market for new homes has totally dried up and large

numbers of those jobs are disappearing. Some of the reasons for this

include high unemployment, a glut of foreclosures on the market and the

tightening of lending standards on home loans. In order for the U.S. to

have anything resembling a healthy economy again, we are going to need a

revival in the sale of new homes. (Read More....)

New

home sales in the United States are on pace to set a brand new all-time

record low in 2011. This will be the third year in a row that new home

sales have set a new record low. Sadly, this is yet another sign that

the U.S. economy continues to grow weaker. Back in 2005, more than four

times as many new homes were being sold as are being sold today. The

home building industry is one of the central pillars of the U.S.

economy, and the fact that we are going to set another new record low

for home sales in 2011 is a really bad sign for those hoping for an

economic recovery. Unlike most of those that work in the financial

industry, those that build new homes produce something of lasting value

for American families. In addition, millions of Americans have

traditionally made a solid living by building and selling new homes.

But today the market for new homes has totally dried up and large

numbers of those jobs are disappearing. Some of the reasons for this

include high unemployment, a glut of foreclosures on the market and the

tightening of lending standards on home loans. In order for the U.S. to

have anything resembling a healthy economy again, we are going to need a

revival in the sale of new homes. (Read More....)[...]

Right

now, interest rates are near historic lows. The U.S. government is

able to borrow gigantic mountains of money for next to nothing. U.S.

consumers are still able to get home loans, car loans and student loans

at ridiculously low interest rates. When this low interest rate

environment changes (and it will), it is going to absolutely devastate

the U.S. economy. Without low interest rates, the U.S. financial system

dies. When it comes to borrowing money, it is the rate of interest

that causes the pain. If you could borrow as much money as you wanted

at a zero rate of interest for the rest of your life you would never,

ever have a debt problem. But when there is a cost to borrowing money

that changes things. The higher the rate of interest goes, the more

painful debt becomes. (Read More....)

Right

now, interest rates are near historic lows. The U.S. government is

able to borrow gigantic mountains of money for next to nothing. U.S.

consumers are still able to get home loans, car loans and student loans

at ridiculously low interest rates. When this low interest rate

environment changes (and it will), it is going to absolutely devastate

the U.S. economy. Without low interest rates, the U.S. financial system

dies. When it comes to borrowing money, it is the rate of interest

that causes the pain. If you could borrow as much money as you wanted

at a zero rate of interest for the rest of your life you would never,

ever have a debt problem. But when there is a cost to borrowing money

that changes things. The higher the rate of interest goes, the more

painful debt becomes. (Read More....)[...]

Unless

you have been asleep or hiding under a rock for the past five years,

you already know that we are experiencing the worst real estate crisis

that the U.S. has ever seen. Home prices in the United States have

fallen 33 percent from the peak of the housing bubble, which is more

than they fell during the Great Depression. Those that decided to buy a

house in 2005 or 2006 are really hurting right now. Just think about

it. Could you imagine paying off a $400,000 mortgage on a home that is

now only worth $250,000? Millions of Americans are now living through

that kind of financial hell. Sadly, most analysts expect U.S. home

prices to go down even further. Despite the "best efforts" of those

running our economy, unemployment is still rampant. The number of

middle class jobs continues to decline

year after year, but it takes at least a middle class income to buy a

decent home. In addition, financial institutions have really tightened

up lending standards and have made it much more difficult to get home

loans. Back during the wild days of the housing bubble, the family cat

could get a zero-down mortgage, but today the pendulum has swung very

far in the other direction and now it is really, really tough to get a

home loan. Meanwhile, the number of foreclosures and distressed

properties continues to soar. So with a ton of homes on the market and

not a lot of buyers the power is firmly in the hands of those looking to

buy a house. (Read More....)

Unless

you have been asleep or hiding under a rock for the past five years,

you already know that we are experiencing the worst real estate crisis

that the U.S. has ever seen. Home prices in the United States have

fallen 33 percent from the peak of the housing bubble, which is more

than they fell during the Great Depression. Those that decided to buy a

house in 2005 or 2006 are really hurting right now. Just think about

it. Could you imagine paying off a $400,000 mortgage on a home that is

now only worth $250,000? Millions of Americans are now living through

that kind of financial hell. Sadly, most analysts expect U.S. home

prices to go down even further. Despite the "best efforts" of those

running our economy, unemployment is still rampant. The number of

middle class jobs continues to decline

year after year, but it takes at least a middle class income to buy a

decent home. In addition, financial institutions have really tightened

up lending standards and have made it much more difficult to get home

loans. Back during the wild days of the housing bubble, the family cat

could get a zero-down mortgage, but today the pendulum has swung very

far in the other direction and now it is really, really tough to get a

home loan. Meanwhile, the number of foreclosures and distressed

properties continues to soar. So with a ton of homes on the market and

not a lot of buyers the power is firmly in the hands of those looking to

buy a house. (Read More....)[...]

If

you make your living by building or selling new homes in the United

States, you might want to consider taking up a different career for a

while. New homes sales in the United States hit yet another new

all-time record low in the month of February, and there are a whole lot

of reasons why new home sales are going to stay extremely low for an

extended period of time. The massive wave of foreclosures that we have

seen has produced a giant glut of unsold homes in the marketplace,

mortgage lenders are making it really hard to get approved for home

loans, unemployment is still rampant and the global economy looks like

it may soon plunge into another major recession. None of those things

is good news for the new home construction industry. The truth is that

we were supposed to have seen new home sales already bounce back by

now. If you look at the historical numbers, new home sales in the U.S. always

increased significantly after the end of every recession since World

War 2. But that did not happen this time. Instead, new home sales have

just continued to decline. This is absolutely unprecedented, and

economists are puzzled. So what is going to happen if the U.S. economy

suffers another major downturn? (Read More....)

If

you make your living by building or selling new homes in the United

States, you might want to consider taking up a different career for a

while. New homes sales in the United States hit yet another new

all-time record low in the month of February, and there are a whole lot

of reasons why new home sales are going to stay extremely low for an

extended period of time. The massive wave of foreclosures that we have

seen has produced a giant glut of unsold homes in the marketplace,

mortgage lenders are making it really hard to get approved for home

loans, unemployment is still rampant and the global economy looks like

it may soon plunge into another major recession. None of those things

is good news for the new home construction industry. The truth is that

we were supposed to have seen new home sales already bounce back by

now. If you look at the historical numbers, new home sales in the U.S. always

increased significantly after the end of every recession since World

War 2. But that did not happen this time. Instead, new home sales have

just continued to decline. This is absolutely unprecedented, and

economists are puzzled. So what is going to happen if the U.S. economy

suffers another major downturn? (Read More....)[...]

Today

there are two very different Americas. In one America, the stock

market is soaring, huge bonuses are taken for granted, the good times

are rolling and people are spending money as if they will be able to

"live the dream" for the rest of their lives. In the other America, the

one where most of the rest of us live, unemployment is rampant, a

million families were kicked out of their homes last year and hordes of

American families are drowning in debt. The gap between the rich and

the poor is bigger today than it ever has been before. In fact, this

article is not so much about "rich vs poor" as it is about "the rich vs

the rest of us". Barack Obama and Ben Bernanke keep touting an

"economic recovery", but the truth is that the only ones that seem to be

benefiting from this recovery are those at the very top of the economic

food chain. (Read More....)

Today

there are two very different Americas. In one America, the stock

market is soaring, huge bonuses are taken for granted, the good times

are rolling and people are spending money as if they will be able to

"live the dream" for the rest of their lives. In the other America, the

one where most of the rest of us live, unemployment is rampant, a

million families were kicked out of their homes last year and hordes of

American families are drowning in debt. The gap between the rich and

the poor is bigger today than it ever has been before. In fact, this

article is not so much about "rich vs poor" as it is about "the rich vs

the rest of us". Barack Obama and Ben Bernanke keep touting an

"economic recovery", but the truth is that the only ones that seem to be

benefiting from this recovery are those at the very top of the economic

food chain. (Read More....) If

you know someone that actually believes that the U.S. economy is in

good shape, just show them the statistics in this article. When you

step back and look at the long-term trends, it is undeniable what is

happening to us. We are in the midst of a horrifying economic decline

that is the result of decades of very bad decisions. 30 years ago, the

U.S. national debt was about one trillion dollars. Today, it is almost

17 trillion dollars. 40 years ago, the total amount of debt in the

United States was about 2 trillion dollars. Today, it is more than 56

trillion dollars. At the same time that we have been running up all of

this debt, our economic infrastructure and our ability to produce wealth

has been absolutely gutted. Since 2001, the United States has lost

more than 56,000 manufacturing facilities and millions of good jobs have

been shipped overseas. Our share of global GDP declined from 31.8

percent in 2001 to 21.6 percent in 2011. The percentage of Americans

that are self-employed is at a record low, and the percentage of

Americans that are dependent on the government is at a record high. The

U.S. economy is a complete and total mess, and it is time that we faced

the truth. (Read More....)

If

you know someone that actually believes that the U.S. economy is in

good shape, just show them the statistics in this article. When you

step back and look at the long-term trends, it is undeniable what is

happening to us. We are in the midst of a horrifying economic decline

that is the result of decades of very bad decisions. 30 years ago, the

U.S. national debt was about one trillion dollars. Today, it is almost

17 trillion dollars. 40 years ago, the total amount of debt in the

United States was about 2 trillion dollars. Today, it is more than 56

trillion dollars. At the same time that we have been running up all of

this debt, our economic infrastructure and our ability to produce wealth

has been absolutely gutted. Since 2001, the United States has lost

more than 56,000 manufacturing facilities and millions of good jobs have

been shipped overseas. Our share of global GDP declined from 31.8

percent in 2001 to 21.6 percent in 2011. The percentage of Americans

that are self-employed is at a record low, and the percentage of

Americans that are dependent on the government is at a record high. The

U.S. economy is a complete and total mess, and it is time that we faced

the truth. (Read More....)[...]

What

in the world is China up to? Over the past several years, the Chinese

government and large Chinese corporations (which are often at least

partially owned by the government) have been systematically buying up

businesses, homes, farmland, real estate, infrastructure and natural

resources all over America. In some cases, China appears to be

attempting to purchase entire communities in one fell swoop. So why is

this happening? Is this some form of "economic colonization" that is

taking place? Some have speculated that China may be intending to

establish "special economic zones" inside the United States modeled

after the very successful Chinese city of Shenzhen.

Back in the 1970s, Shenzhen was just a very small fishing village, but

now it is a sprawling metropolis of over 14 million people. Initially,

these "special economic zones" were only established within China, but now the Chinese government has been buying huge tracts of land in foreign countries such as Nigeria

and establishing special economic zones in those nations. So could

such a thing actually happen in America? Well, according to Dr. Jerome Corsi,

a plan being pushed by the Chinese Central Bank would set up

"development zones" in the United States that would allow China to

"establish Chinese-owned businesses and bring in its citizens to the

U.S. to work." Under the plan, some of the $1.17 trillion

that the U.S. owes China would be converted from debt to "equity". As a

result, "China would own U.S. businesses, U.S. infrastructure and U.S.

high-value land, all with a U.S. government guarantee against loss."

Does all of this sound far-fetched? Well, it isn't. In fact, the

economic colonization of America is already far more advanced than most

Americans would dare to imagine. (Read More....)

What

in the world is China up to? Over the past several years, the Chinese

government and large Chinese corporations (which are often at least

partially owned by the government) have been systematically buying up

businesses, homes, farmland, real estate, infrastructure and natural

resources all over America. In some cases, China appears to be

attempting to purchase entire communities in one fell swoop. So why is

this happening? Is this some form of "economic colonization" that is

taking place? Some have speculated that China may be intending to

establish "special economic zones" inside the United States modeled

after the very successful Chinese city of Shenzhen.

Back in the 1970s, Shenzhen was just a very small fishing village, but

now it is a sprawling metropolis of over 14 million people. Initially,

these "special economic zones" were only established within China, but now the Chinese government has been buying huge tracts of land in foreign countries such as Nigeria

and establishing special economic zones in those nations. So could

such a thing actually happen in America? Well, according to Dr. Jerome Corsi,

a plan being pushed by the Chinese Central Bank would set up

"development zones" in the United States that would allow China to

"establish Chinese-owned businesses and bring in its citizens to the

U.S. to work." Under the plan, some of the $1.17 trillion

that the U.S. owes China would be converted from debt to "equity". As a

result, "China would own U.S. businesses, U.S. infrastructure and U.S.

high-value land, all with a U.S. government guarantee against loss."

Does all of this sound far-fetched? Well, it isn't. In fact, the

economic colonization of America is already far more advanced than most

Americans would dare to imagine. (Read More....)[...]

This

is the time of the year when Americans run out to their favorite retail

stores and fill up their shopping carts with lots of cheap plastic crap

made by workers in foreign countries where it is legal to pay slave

labor wages. By doing this, the American people are actively

participating in the destruction of the U.S. economy. You see, buying

products that are made in America is not just a matter of national

pride. It is a matter of national survival. If we do not support

American workers, they are going to continue to see their jobs shipped

out of the country. If we do not support American businesses, they are

going to continue to die off at a staggering rate. Last year, the

United States had a trade deficit with the rest of the world of 558

billion dollars. More than half a trillion dollars that could have gone

into the pockets of U.S. workers and U.S. businesses went overseas

instead. If that money had stayed in the country, taxes would have been

paid on that mountain of cash and our local, state and federal

government debt problems would not be as severe. As a result of our

massive trade imbalance, we have lost tens of thousands of businesses,

millions of jobs and trillions of dollars of national wealth. Both

major political parties have sold us out on these issues, and we are

getting poorer as a nation with each passing day. We desperately need a

resurgence of economic patriotism in the United States before it is too

late. (Read More....)

This

is the time of the year when Americans run out to their favorite retail

stores and fill up their shopping carts with lots of cheap plastic crap

made by workers in foreign countries where it is legal to pay slave

labor wages. By doing this, the American people are actively

participating in the destruction of the U.S. economy. You see, buying

products that are made in America is not just a matter of national

pride. It is a matter of national survival. If we do not support

American workers, they are going to continue to see their jobs shipped

out of the country. If we do not support American businesses, they are

going to continue to die off at a staggering rate. Last year, the

United States had a trade deficit with the rest of the world of 558

billion dollars. More than half a trillion dollars that could have gone

into the pockets of U.S. workers and U.S. businesses went overseas

instead. If that money had stayed in the country, taxes would have been

paid on that mountain of cash and our local, state and federal

government debt problems would not be as severe. As a result of our

massive trade imbalance, we have lost tens of thousands of businesses,

millions of jobs and trillions of dollars of national wealth. Both

major political parties have sold us out on these issues, and we are

getting poorer as a nation with each passing day. We desperately need a

resurgence of economic patriotism in the United States before it is too

late. (Read More....)[...]

Either

way this election turns out, American jobs are going to continue to get

slaughtered by the millions. During this campaign, Mitt Romney and

Barack Obama have both attempted to portray each other as the "outsourcer in chief".

Unfortunately, they are both right. Barack Obama and Mitt Romney have

both participated in the outsourcing of American jobs, and both are

openly admitting to the American people that they favor the emerging one

world economic system which will continue to destroy millions of

American jobs. In fact, they argue with each other about which of them

will be more aggressive in pursuing more "free trade" agreements over

the next four years. Unfortunately, the "free trade" agreements that

the U.S. government enters into are never "fair trade" agreements. As a

result, over the past decade we have lost tens of thousands of

businesses, millions of jobs and trillions of dollars of national

wealth. This year alone, we will buy about half a trillion dollars more

stuff from the rest of the world than they will buy from us. This

trade deficit will be about 7 times larger than the trade deficit of any

other nation on earth. Our economy will continue to bleed jobs at a

horrifying pace, but Obama and Romney insist that the answer to our

problems is even more "free trade". What makes all of this even more

dreadful is that most Americans continue to fall for this nonsense. (Read More....)

Either

way this election turns out, American jobs are going to continue to get

slaughtered by the millions. During this campaign, Mitt Romney and

Barack Obama have both attempted to portray each other as the "outsourcer in chief".

Unfortunately, they are both right. Barack Obama and Mitt Romney have

both participated in the outsourcing of American jobs, and both are

openly admitting to the American people that they favor the emerging one

world economic system which will continue to destroy millions of

American jobs. In fact, they argue with each other about which of them

will be more aggressive in pursuing more "free trade" agreements over

the next four years. Unfortunately, the "free trade" agreements that

the U.S. government enters into are never "fair trade" agreements. As a

result, over the past decade we have lost tens of thousands of

businesses, millions of jobs and trillions of dollars of national

wealth. This year alone, we will buy about half a trillion dollars more

stuff from the rest of the world than they will buy from us. This

trade deficit will be about 7 times larger than the trade deficit of any

other nation on earth. Our economy will continue to bleed jobs at a

horrifying pace, but Obama and Romney insist that the answer to our

problems is even more "free trade". What makes all of this even more

dreadful is that most Americans continue to fall for this nonsense. (Read More....)[...]

The

mainstream media in the United States is almost totally ignoring one of

the most important trends in global economics. This trend is going to

cause the value of the U.S. dollar to fall dramatically and it is going

to cause the cost of living in the United States to go way up. Right

now, the U.S. dollar is the primary reserve currency of the world. Even

though that status has been chipped away at in recent years, U.S.

dollars still make up more than 60 percent

of all foreign currency reserves in the world. Most international

trade (including the buying and selling of oil) is conducted in U.S.

dollars, and this gives the United States a tremendous economic

advantage. Since so much trade is done in dollars, there is a constant

demand for more dollars all over the globe from countries that need them

for trading purposes. So the Federal Reserve is able to flood our

financial system with dollars without it causing a tremendous amount of

inflation because the rest of the world ends up soaking up a lot of

those dollars. But now that is changing. China and Russia have been

spearheading a movement to shift away from using the U.S. dollar in

international trade. At the moment, the shift is happening gradually,

but at some point a tipping point will come (for example if Saudi Arabia

were to declare that it will no longer take U.S. dollars for oil) and

the entire global financial system is going to change. When that

tipping point comes the global demand for U.S. dollars is going to

absolutely plummet and nightmarish inflation will come to the United

States. If such a scenario sounds far out to you, then you have not

been paying attention. In fact, China and Russia have been working very

hard to move us toward exactly such a scenario. (Read More....)

The

mainstream media in the United States is almost totally ignoring one of

the most important trends in global economics. This trend is going to

cause the value of the U.S. dollar to fall dramatically and it is going

to cause the cost of living in the United States to go way up. Right

now, the U.S. dollar is the primary reserve currency of the world. Even

though that status has been chipped away at in recent years, U.S.

dollars still make up more than 60 percent

of all foreign currency reserves in the world. Most international

trade (including the buying and selling of oil) is conducted in U.S.

dollars, and this gives the United States a tremendous economic

advantage. Since so much trade is done in dollars, there is a constant

demand for more dollars all over the globe from countries that need them

for trading purposes. So the Federal Reserve is able to flood our

financial system with dollars without it causing a tremendous amount of

inflation because the rest of the world ends up soaking up a lot of

those dollars. But now that is changing. China and Russia have been

spearheading a movement to shift away from using the U.S. dollar in

international trade. At the moment, the shift is happening gradually,

but at some point a tipping point will come (for example if Saudi Arabia

were to declare that it will no longer take U.S. dollars for oil) and

the entire global financial system is going to change. When that

tipping point comes the global demand for U.S. dollars is going to

absolutely plummet and nightmarish inflation will come to the United

States. If such a scenario sounds far out to you, then you have not

been paying attention. In fact, China and Russia have been working very

hard to move us toward exactly such a scenario. (Read More....)Government Debt

Anyone

that thinks that the U.S. economy can keep going along like this is

absolutely crazy. We are in the terminal phase of an unprecedented debt

spiral which has allowed us to live far, far beyond our means for the

last several decades. Unfortunately, all debt spirals eventually end,

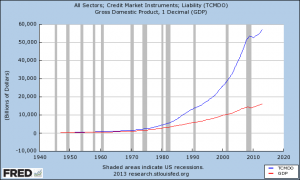

and they usually do so in a very disorderly manner. The chart that you

are about to see is one of my favorite economic charts. It compares the

growth of U.S. GDP to the growth of total debt in the United States.

Yes, U.S. GDP has certainly grown at a decent pace over the years, but

our total debt has absolutely exploded. 40 years ago, the total amount

of debt in our system (government debt + corporate debt + consumer debt,

etc.) was about 2 trillion dollars. Today it has grown to more than 56 trillion dollars.

Our debt has grown at a much, much faster rate than our economy has,

and there is no way in the world that we will be able to continue to do

that for long. (Read More....)

Anyone

that thinks that the U.S. economy can keep going along like this is

absolutely crazy. We are in the terminal phase of an unprecedented debt

spiral which has allowed us to live far, far beyond our means for the

last several decades. Unfortunately, all debt spirals eventually end,

and they usually do so in a very disorderly manner. The chart that you

are about to see is one of my favorite economic charts. It compares the

growth of U.S. GDP to the growth of total debt in the United States.

Yes, U.S. GDP has certainly grown at a decent pace over the years, but

our total debt has absolutely exploded. 40 years ago, the total amount

of debt in our system (government debt + corporate debt + consumer debt,

etc.) was about 2 trillion dollars. Today it has grown to more than 56 trillion dollars.

Our debt has grown at a much, much faster rate than our economy has,

and there is no way in the world that we will be able to continue to do

that for long. (Read More....)[...]

When

you add maturing debt to the new debt that the federal government is

accumulating, the total is quite eye catching. You see, the truth is

that the U.S. government must not only borrow enough money to fund

government spending for this year, it must also "roll over" existing

debt that has reached maturity. Of course the government never actually

pays any of that debt off. Instead, it essentially takes out new debts

to cover the old ones. So the U.S. government is actually borrowing

far more money each year than most Americans realize. For fiscal year

2013, the U.S. budget deficit will be about $845 billion, but on top of that the government will also have to borrow about 3 trillion dollars

to pay off old debt that is maturing. Overall, the U.S. government

will borrow close to 4 trillion dollars this year, and that number will

likely be even higher next year. That is not going to cause a crisis as

long as interest rates stay super low, but if interest rates begin to rise substantially, the game will change dramatically. (Read More....)

When

you add maturing debt to the new debt that the federal government is

accumulating, the total is quite eye catching. You see, the truth is

that the U.S. government must not only borrow enough money to fund